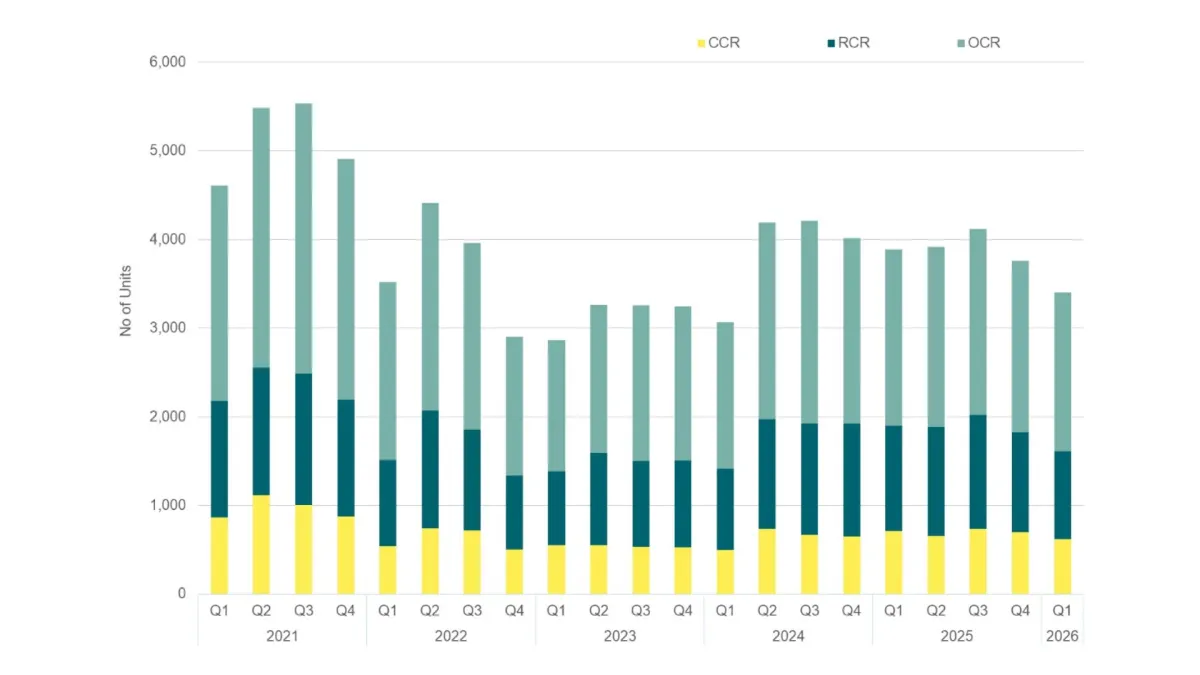

Singapore’s secondary private housing market weakened further in the first quarter of 2026, with resale transactions falling 9.6% quarter-on-quarter as buyers increasingly shifted toward newly launched residential projects.

According to a report by Savills Research, the decline marked the second consecutive quarterly contraction in Singapore’s secondary home sales market following an earlier 8.7% drop in the fourth quarter of 2025.

The downturn reflects broader cooling activity across the city-state’s property market amid:

- Softer buyer demand

- Reduced resale supply

- Fewer housing completions

- Growing competition from primary market launches

Singapore’s Resale Housing Market Loses Momentum

The latest data shows Singapore’s secondary residential market continues struggling to regain the momentum seen during the post-pandemic property rebound.

Secondary home sales had previously peaked between:

- Q2 and Q3 2021

when transaction volumes exceeded:

- 5,000 units quarterly

However, volumes weakened sharply throughout:

- 2022

- 2023

before partially recovering in:

- Q2 and Q3 2024

when quarterly transactions again surpassed:

- 4,000 units.

Market activity stabilized somewhat during 2025 before weakening again in early 2026.

Buyers Shift Toward New Launches

One of the biggest drivers behind the resale slowdown has been growing demand for:

- Primary residential launches

Developers have increasingly introduced new projects that attract buyers with:

- Modern amenities

- Flexible payment structures

- Promotional incentives

- Newer facilities

- Energy-efficient features

This has diverted some purchasing activity away from older resale units.

The report suggests many buyers now prefer:

- Newly completed condominiums

- Integrated developments

- Newly launched suburban projects

despite higher pricing in some segments.

Core Central Region Records Sharpest Decline

The:

- Core Central Region (CCR)

recorded the steepest quarter-on-quarter decline among Singapore’s three key market segments.

Resale transactions in the CCR fell:

- 11.7% to 616 units

The segment includes many of Singapore’s:

- Prime luxury districts

- High-end condominiums

- Central business area residences

The Q1 performance represented the lowest resale volume for the CCR since:

- Q1 2024

when only:

- 499 units

were transacted.

Rest of Central Region Also Weakens

The:

- Rest of Central Region (RCR)

also experienced significant contraction.

Transactions declined:

- 11.4% to 996 units

This marked the segment’s weakest quarterly resale performance since:

- Q1 2024

when volumes reached:

- 913 units.

The RCR typically includes:

- City fringe properties

- Mid-tier condominiums

- Popular suburban-adjacent districts

which are often highly competitive among owner-occupiers and investors.

Outside Central Region Remains Most Active

The:

- Outside Central Region (OCR)

continued accounting for the largest share of secondary transactions despite slowing activity.

Sales in the OCR declined:

- 7.7% to 1,788 units

from:

- 1,937 units in the previous quarter.

Even with the decline, the OCR remained more resilient than other segments because of:

- Lower entry prices

- Greater affordability

- Stronger mass-market demand

Savills noted that buyers continue viewing suburban projects as relatively attractive compared with rising prices in newly launched developments.

Affordability Becoming Bigger Market Factor

Affordability concerns increasingly influence buyer decisions across Singapore’s housing market.

Higher financing costs, elevated property prices, and cautious economic sentiment have pushed many buyers toward:

- Smaller units

- Suburban properties

- Lower-priced resale homes

At the same time, new launches in central areas have become increasingly expensive, further limiting accessibility for some buyers.

The affordability gap between:

- Prime properties

- Mass-market suburban housing

continues widening.

Singapore Property Market Facing More Balanced Conditions

The latest data may signal a broader normalization within Singapore’s residential property market after years of strong post-pandemic growth.

Government cooling measures, higher borrowing costs, and tighter financing conditions have all contributed to:

- Moderating demand

- Slowing speculative activity

- Stabilizing transaction volumes

Singapore authorities have repeatedly emphasized the importance of:

- Sustainable housing growth

- Financial stability

- Controlled property inflation

Supply Constraints Also Affecting Resale Activity

The report also highlighted reduced resale inventory and fewer home completions as contributing factors behind weaker transaction volumes.

Limited resale supply can restrict market activity because:

- Buyers face fewer choices

- Sellers hold properties longer

- Competition intensifies for available units

At the same time, developers continue prioritizing new launches in strategic locations, pulling more demand into the primary market.

Investors Continue Watching Singapore Closely

Despite the slowdown, Singapore remains one of Asia’s most closely watched residential property markets because of:

- Political stability

- Strong legal framework

- High-income economy

- International investor demand

- Limited land supply

The city-state continues attracting:

- Foreign investors

- Regional wealth

- Institutional capital

- Family office investments

especially in premium residential districts.

Luxury Segment Facing More Caution

The sharper decline in the:

- Core Central Region

may also indicate increasing caution within the luxury market.

High-end buyers are becoming more selective amid:

- Global economic uncertainty

- Geopolitical tensions

- Interest rate volatility

- Wealth preservation concerns

Luxury property activity remains highly sensitive to:

- International capital flows

- Currency movements

- Investor confidence

Singapore’s Housing Market Still Structurally Strong

While transaction volumes weakened, analysts continue viewing Singapore’s long-term property fundamentals as relatively resilient because of:

- Limited land availability

- Population growth

- Strong infrastructure

- Stable governance

- Regional financial hub status

The market slowdown currently appears more linked to:

- Demand moderation

- Buyer caution

- Market rebalancing

rather than systemic weakness.

Frequently Asked Questions

How much did secondary home sales fall in Singapore?

Secondary private residential sales fell 9.6% quarter-on-quarter in Q1 2026.

Which market segment declined the most?

The Core Central Region recorded the largest decline at 11.7%.

Why are resale transactions weakening?

Factors include:

- Weaker buyer demand

- Shift toward new launches

- Reduced resale supply

- Higher property prices

Which segment remains most active?

The Outside Central Region continues recording the highest transaction volumes.

Is Singapore’s property market weakening overall?

The market is moderating after strong post-pandemic growth, but long-term fundamentals remain relatively stable.

Conclusion

Singapore’s secondary residential property market entered 2026 on a weaker footing as softer buyer demand, limited resale supply, and competition from new launches continued weighing on transaction activity.

While the decline reflects a cooling market environment, Singapore’s broader housing sector remains supported by strong structural fundamentals, limited land supply, and continued investor interest.

As affordability pressures and shifting buyer preferences reshape the market, developers, investors, and policymakers will be closely monitoring whether the slowdown signals a temporary adjustment or the start of a longer market recalibration.